Dividends have the potential to provide a significant source of income for our stock portfolios. Since the S&P 500 was established in 1926, capital appreciation has, on average, contributed 68% of the total return achieved by the S&P 500. Dividend income has contributed the other 32%. An alternate way of thinking about this is that of the average annual return of +7.0% over the years, +4.5% was from capital appreciation and +2.2% came from dividends.

Since dividend income represents almost one-third of stocks total return potential over time, I wanted to develop a way to explicitly consider capturing dividend income as part of our Covered Calls investing process. So, let's consider these concepts that will help us determine what specific criteria we should use in developing a Covered Calls "Dividend Capture Strategy":

1. We prefer out-of-the-money strike prices when our Overall Market Meter sentiment is Bullish or Slightly Bullish, near-the-money when Neutral, and in-the-money when Bearish or Slightly Bearish.

2. Since dividends reduce the stock price by the amount of the dividend at market open on the ex-dividend date (remember: "there's no such thing as a free lunch in investing"), Covered Calls with in-the-money strike prices provide the best opportunity to both capture the dividend on the ex-dividend date but also to be in-the-money and therefore be assigned on the options expiration date. So, we will normally obtain our best advantage using a "Dividend Capture Strategy" when we establish in-the-money Covered Calls positions (which would be when our market sentiment is either Slightly Bearish, Bearish, or even sometimes when Neutral).

3. We prefer short-duration (one month or less) Covered Calls positions since they provide higher potential annualized-return-on-investment (aroi) results than Covered Call positions of longer durations.

4. For any company that we are Bullish on and would consider investing in, and which is also a dividend-paying company, we prefer to be invested in that company on its ex-dividend date (so we will capture the dividend).

5. Most companies pay quarterly dividends, so we prefer to establish positions during the one month each quarter when that particular company goes ex-dividend. Conversely, we can decide to avoid positions in that same company during the two months each quarter when they don't go ex-dividend--and instead switch our cash to other companies that do go ex-dividend in those months. When we hold a position for a month or less and also capture its quarterly dividend, we effectively increase its equivalent-annualized-dividend-yield since the quarterly dividend income received is not spread over the entire 3 month period but rather is received only over the total number of days we hold the position during its ex-dividend month.

6. On the one hand, Call options owners will almost always consider exercising their Calls on the final business day prior to the ex-dividend date (to purchase the stock in order to capture the following day's dividend) and they will normally do so only when the stock price is deep-in-the-money such that the time value remaining then in the Calls is close to $0.00.

7. For Covered Calls with intervening ex-dividend dates (i.e. ex-dividends prior to the options expiration date) we can evaluate the potential annualized-return-on-investment (aroi) before we enter our Covered Calls order under two scenarios: (1) if it is assigned early (on the day prior to the ex-dividend date); or (2) if it is assigned on the options expiration date. To avoid being disappointed when we are assigned early and we therefore miss out on the dividend, we prefer that the aroi for early assignment is greater than the aroi if we capture the dividend and the position is instead assigned on the options expiration date. Fortunately, we can calculate the potential aroi if assigned under both of these scenarios before we enter any Covered Calls order and we can choose to establish the position on days that achieve this desirable objective.

8. We like to avoid the stock price volatility that normally occurs when quarterly earnings reports are released. So before establishing a new Covered Calls position, we should always check for the the next earnings reporting date and avoid positions in companies with earnings reports prior to the potential options expiration date.

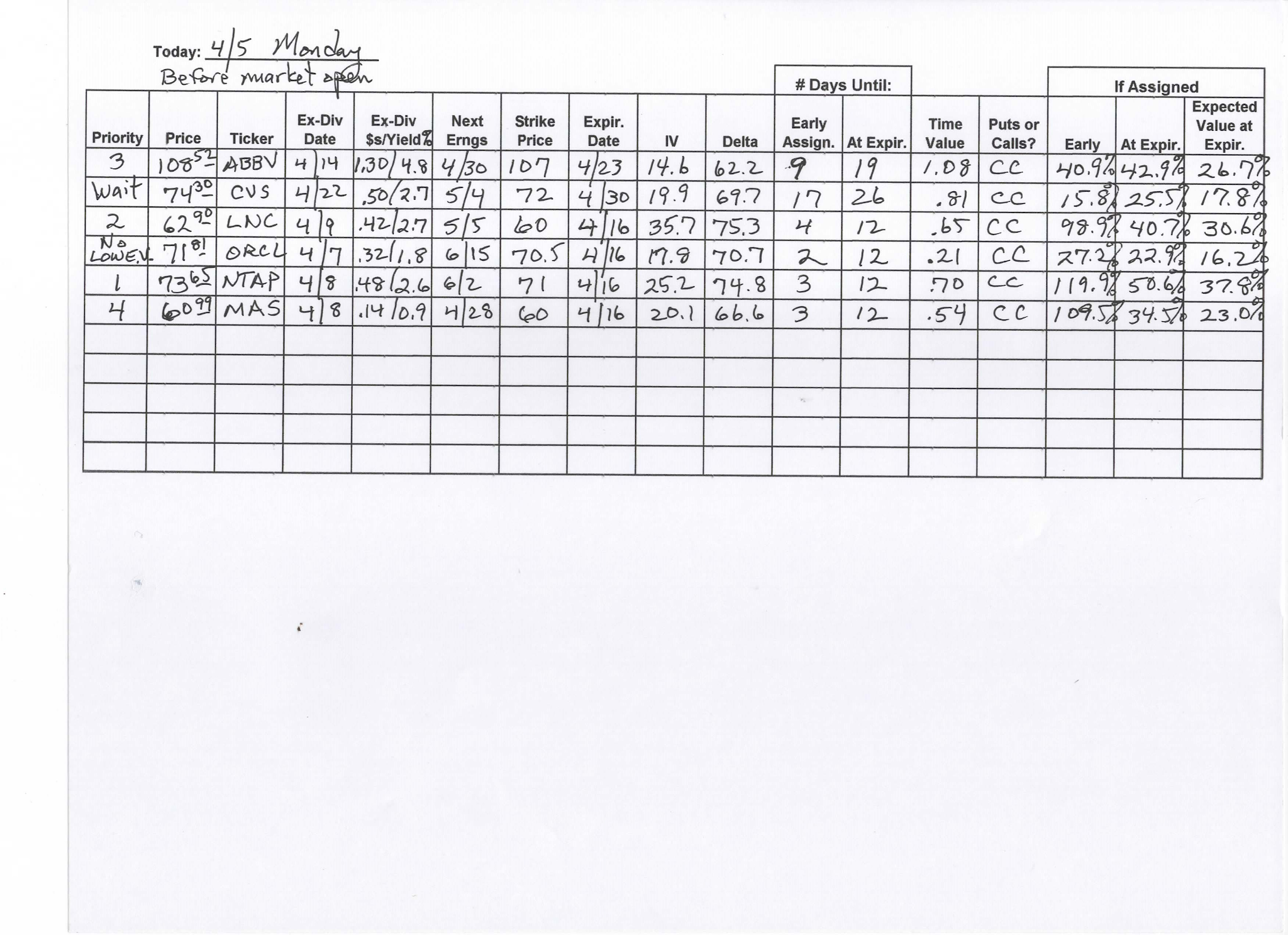

Over several years, I have developed a list of rules to use prior to establishing a Covered Calls position with a dividend-paying company. I have continued to modify the list to a point now that I believe this list of nine criteria (my "Dividend Capture Strategy") provides a solid framework for achieving market-beating results when applying the Covered Calls investing strategy to dividend-paying companies. Here is an example of the application of these nine criteria to a recent Covered Calls position in CVS Health (see detailed blog post here):

In this CVS example for criteria #8 and #9 above, you can see how the annualized-return-on-investment potential for early assignment of +45.4% is greater than the +36.8% aroi if assigned on the options expiration date. So, as stated in concept #7 in the article above, "To avoid being disappointed when we are assigned early and we therefore miss out on the dividend, we prefer the at aroi for early assignment is greater than the aroi if we capture the dividend and the position is instead assigned on the options expiration date."

Many of the concepts described above are included as part of a more comprehensive blog post I made in 2021 that identified twelve "Investing Edges" we can exploit as Covered Calls investors that enable us to outperform typical stock market benchmarks (such as the S&P 500). I encourage you to undertake a careful reading of this article when you have time to devote to it: Exploiting Our Covered Calls Investing "Edges".

This post is more in-depth than most. My hope is that it will be useful to you. I apologize if it is written in a way that is not as clear as it could be; so please feel free to email me at partlow@cox.net if I can clarify something that you have further question(s) about. Replying to your questions will help me edit this post further in order to improve its completeness and clarity.

Best Wishes and Godspeed,

Jeff Partlow

The Covered Calls Advisor